Who is the Australian property market’s typical investor?

Contrary to the image a property investor might conjure up – a wealthy full-time property speculator – most residential investors in Australia don’t actually rely on it as their primary source of income.

In reality, Australia’s residential investment market is dominated by people who, having bought their own home, have moved onto buying an investment property. These small-scale investors own 83 per cent of all investment properties.

Previous research shows that real estate investors tend to be married, wealthy males with high income and full-time employment.

A typical rental housing investor is a high-income earner or family partnership, owning one or two dwellings as an extra income source. The probability of becoming a residential investor tends to increase with age and homeowner status, but declines after the age of 65.

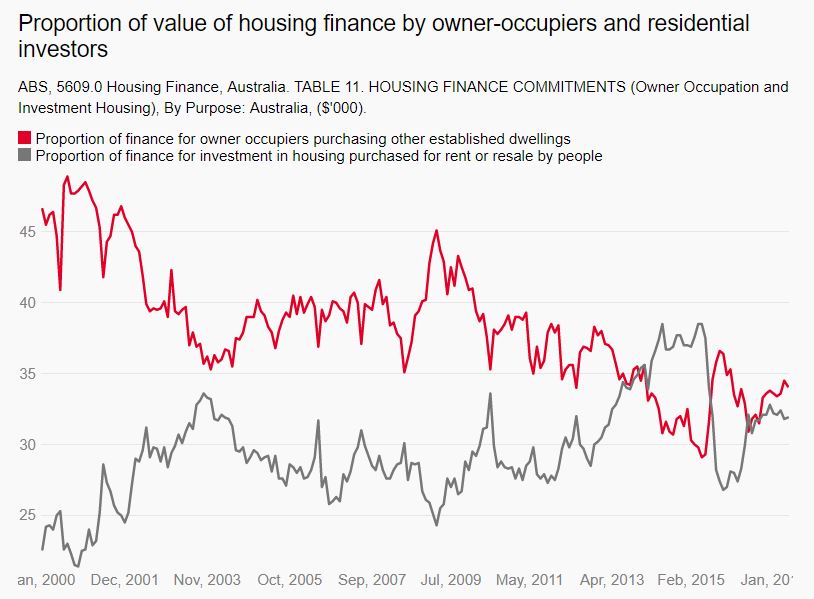

With home ownership rates in Australia at around 70 per cent, the Australian Bureau of Statistics (ABS) reports that residential investment represents, on average, 35 per cent of all housing finance, while the rest are all owner-occupiers. This means residential investment is an important part of the mortgage market and banking system.

Most residential investment is centred around rent or resale; only a small proportion goes on construction of new homes. And residential investment by corporations or big companies represents only 8 per cent of the market.

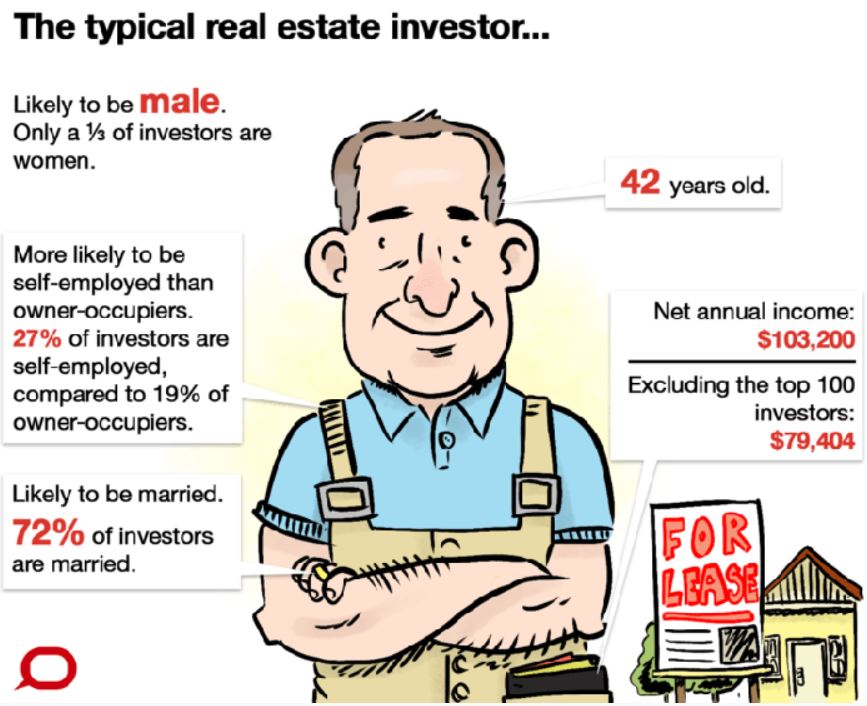

Private data from a major mortgage provider used in my research (for the period 2003-09) reveals what the typical real estate investor looks like. They are on average 42 years old, 72 per cent are married, and fewer than two-thirds of investors get finance with a co-borrower. Only a third of investors are female.

According to the same data, residential investors have an average net monthly income of $8,600, or $103,200 a year. But if we exclude the 100 investors with a net monthly income over $100,000, the average net monthly income becomes $6,617, or $79,404 a year.

Residential investors, financing the property with a mortgage, have on average $934,091 in net wealth (50 per cent of investors have $581,541 in net wealth). Some of them have diverse portfolios; six sources of investors also own shares with an average value of $4,884.

The data also show that direct residential investors are mainly professionals, in management positions, small business-owners, or workers with a skilled trade. Overall, 27 per cent are self-employed, relative to the 19 per cent of self-employed owner-occupiers.

Where they invest

The data reveal that direct residential investors invest mainly on existing houses, as do owner-occupiers when buying a property. The ABS reports only 3 per cent of investors’ financial commitments are destined for construction of new dwellings.

Our data shows that residential investors are more willing to invest interstate or in a different postcode than owner-occupiers. While almost half of residential investors invest in a property located in a different postcode to where they live, 11 per cent of residential investors buy properties in states other than the state where they live.

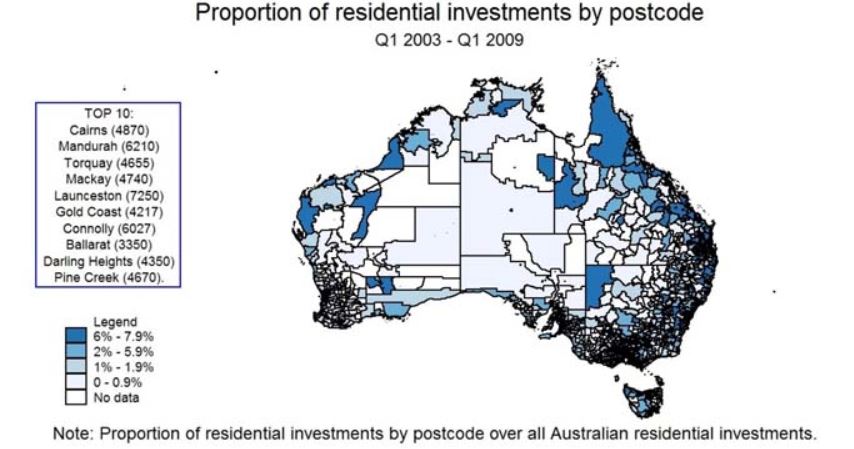

Most residential investors choose rural and regional areas to invest. Many residential investors choose to buy property in big metropolitan cities like Sydney and Melbourne.

However, the top 10 postcodes chosen by residential investors to buy property (between 2003 and 2009) include Cairns (QLD), Mandurah (WA), Torquay (VIC), Mackay (QLD) and Launceston (TAS).

Why do they invest?

Our research shows the main reasons for accessing finance to buy a house, other than to live in it, are income and wealth accumulation.

Some investors invest because they see it as a long-term, secure, “bricks and mortar” investment. To these investors other types of assets (such as shares and bonds) may seem harder to understand and it may be more costly to enter these markets.

A proportion of real estate investors see it as a source of permanent income, while others speculate on the potential capital gains in real estate and invest expecting to increase their wealth.

This reason becomes more prominent during periods of strong house price appreciation. For example, between 2003 and 2009 year-to-year average house price inflation has been 8.9 per cent.

Academics have also argued that the Australian taxation system motivates — rather than facilitates — housing investment, as investors are able to access 50 per cent deduction on capital gains and negative gearing. Another motivator to invest in real estate may be more mortgage finance access; for example, between 2003 and 2009 the average 12-month housing credit growth has been of 14.6 per cent.

Of course there are other reasons to invest, such as moving up or down and maintaining other property as an investment, or getting a holiday home and keeping it as an investment too. There are also “unintentional” real estate investors that may have inherited or acquired property.

Most residential investors are your average Australians, who invest in rural or regional areas as a secondary source of income and to gain equity. So when thinking about who is the typical Australian retail investor, you could probably look at your neighbour.